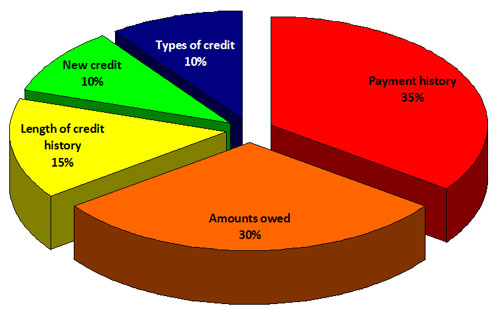

One of the key figures in all of personal finance, your credit score could be the difference between approval and rejection when it comes to applying for any form of finance, credit card, loan or mortgage. Even expenditures that may seem irrelevant such as gym memberships, direct debits and subscriptions – to a magazine or online service such as Netflix or Spotify – can change your score for better or worse, so it’s well worth knowing the ins and outs of credit before you get to the stage of wanting a higher score.

In short, your credit score measures the risk a lender would face in borrowing you money in numerical form, standardising your financial trustworthiness and reliability to make it easier for banks to make informed decisions on who they’re doing business with. The higher your score, the lower the risk you represent, which in turn makes you far more likely to gain approval for any additional funding that you may be seeking. If you do have a poor score, there are ways to improve it over time, and there are bank accounts specifically available for those who don’t wish for their credit score to be accessed as part of the approval process.

While this may not seem like a priority before you have long term financial commitments, when the time does come to buy or rent a property, invest in a new car or seek a loan, it will suddenly be of the upmost importance. Even insurance companies will check your score before allocating your premiums. Having the knowledge to be proactively prudent should help the management of your personal finances improve immeasurably, which will benefit you for years ahead.

How Can Checking My Credit Score Affect My Score?

There are two ways your credit is checked – hard or soft. In a hard check, the inquiry can exist on your credit report for two-years, but will only count toward the calculation of your score for the first 12 months. If you feel that a company have pulled your credit history in a fashion or for a reason you’re in disagreement with, you can challenge those to try and have it erased from your record if successful.

What Is A Soft Check?

More common than the hard check, a soft check won’t count against your score or be retained on your report. Used when you’re looking at your own records and figures, and by prospective employers or someone in the process of approving your for a loan or finance, these are often part of the pre-approval proves where long-term financial commitments are concerned.